It’s been four weeks of pandemonium in the market.

Saturday, 21 Mar 2020, By TEE LIN SAY

Just a month ago, markets across the globe, particularly the Dow Jones and the S&P 500 were at all-time highs.

How things have change so drastically in a matter of weeks.

Covid-19 has gripped the world, not just with its ability to spread disease quickly, but also to replicate fear and terror.

Governments around the world have hurriedly launched their respective stimulus packages to attempt to fight the contagion and collateral damage left in its aftermath.

However, judging by how financial markets have been hit by circuit breakers, limit-downs or even shut down, it’s safe to say that mass panic is the emotion ruling the day.

Who is even thinking about valuations any more?

The Dow Jones has fallen 32.7% from its peak of 29,569 on Feb 12, while the S&P 500 has also fallen 29.3%% from its peak of 3,386 on Feb 19.

Malaysia was not spared.

The FBM KLCI has been floundering since the 2014 general election. Since its peak of 1,887 on April 20,2018, the index has been on a slow downtrend.

From that peak, the market is down some 35% at the 1,219 level on Thursday. On a year-to-date basis, the FBM KLCI is down 23.7%.

In early February, it was the 1,500 level that was the support for the local index.

By end-February, it had to be the 1,400 level. By March 16, the 1,300 level was breached and the 1,100 level could be the next stop.

The reasons for the FBM KLCI free fall are the margin calls and force-selling. Those who cannot cover their margin calls are forced to sell and the stock goes to a new low. This, in turn, triggers the margin call again, where prices again hit new lows, and more investors are affected. It’s a vicious downward spiral until the last of the weak sellers have been taken out.

What the market needs now is stability. It doesn’t need to go up. It just needs the margin calls to be contained, if not stopped.

So, at the market’s current level, are we close to that point?

Volatile market

Former investment banker Ian Yoong said neither he nor anyone else knows whether equity prices have reached rock bottom.

“However, what is patently clear is that tremendous values have emerged after the recent collapse. For example, Maybank, CIMB and Public Bank, the three leading Malaysian financial institutions, are trading at historical price earning ratios of nine times, seven times and nine times respectively. Dividend yields of Maybank and CIMB are between 7% and 8%.

“There is so much value in well managed listed companies that it would be a fantastic time for major shareholders to take their companies private, ” says Yoong.

UOB Kay Hian research head Vincent Khoo says that so much has been priced into the market. Nonetheless, markets could still fall.

“There could be another selldown. Whenever we think we’ve reached the bottom, another selldown happens and we get a new fresh low.”

“It’s no longer about valuations but liquidity considerations, amid a sharp global rise in credit risks and uncertain duration of the Covid-19 lockdown-induced global recession. Governments of impacted countries need to swiftly assist companies which are facing liquidity issues” says Khoo.

“Malaysia’s restricted movement may have backfired, and perhaps even compounded the situation, as many citizens did not practise home-quarantine. Hence, there is now a fear that this two weeks of restricted movement could be extended. So, the market is pummelled by a sum of all fears. It is greatly impacted by the restricted movement on businesses and what happens if it is extended, ” said Khoo.

He added that there isn’t a precedent to what is happening, and people are still panicking.

Khoo’s advice for investors who are already invested (caught) in the market, is to just endure this period, so long as the companies can financially withstand the business lull until the global Covid-19 infection peaks.

“The government needs to be resolute and swift, particularly in helping the SMEs, otherwise many people will be out of jobs. As it is, there have already been news on retrenchment and workers being made redundant over the last few weeks, ” says Khoo.

Former investment banker Ian Yoong said that the collapse in share prices is because of panic selling, expectations of further falls in prices, short selling, forced selling of margin accounts and selling because of fund redemptions.

“Investors sell what they can sell, not what they want to sell. Euphoric and illogical selling, ” says Yoong.

Yoong said that the negativity of this current crisis far exceeds the Global Financial Crisis of 2008. The current crisis approximates that of the Asian Financial Crisis of 1997.

“Many fortunes were lost and many fortunes made at every crisis, ” says Yoong.

The main stages in a market cycle are optimism, excitement, euphoria, anxiety, denial, fear, capitulation, despondency, hope and relief.

“Global equity markets is at the capitulation level or close to it. This is indeed a once in a decade or possibly lifetime opportunity to make our fortunes. Let calm heads prevail when everyone else is losing theirs, ” says Yoong.

Using history as a guide

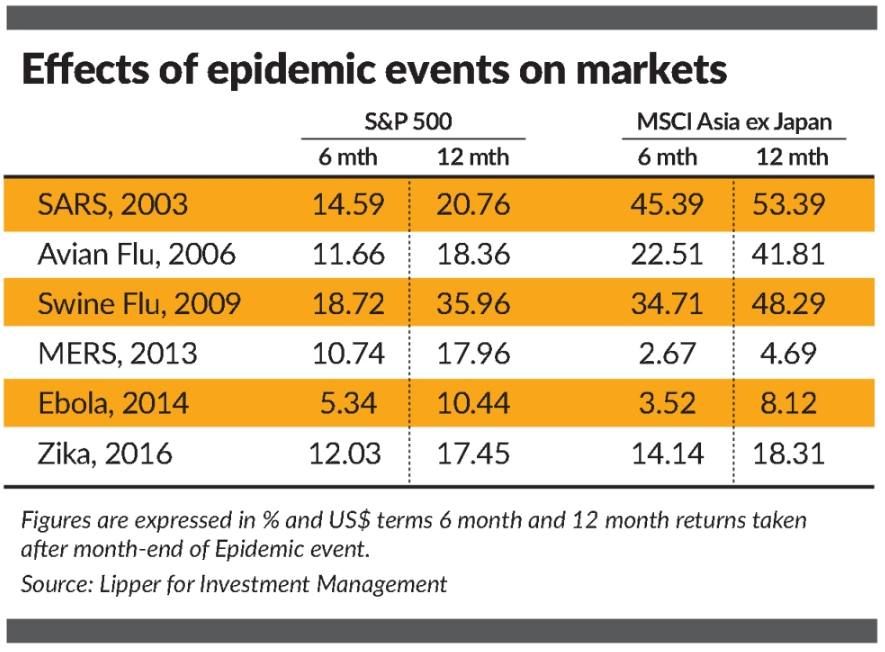

In analysing the effects that past epidemics and pandemics have on global markets, Areca Capital Sdn Bhd chief executive officer Danny Wong has one conclusion:

“Pandemics come and go. Markets eventually move past them and carry on. As historical precedence shows, markets even rebounded stronger (see chart), ”

“We are now at the stage where the majority of investors have started to panic and dumped their assets. For the astute and long-term investor, this is an opportunity. It is a very rare opportunity to be able to pick up stocks at crisis-level valuation, without being in an actual financial crisis, ” says Wong.

Besides that, Wong points out that foreign holdings are at an all-time low.

Data recorded since 2010 shows that the cumulative net inflow of foreign funds into the equity market stands at (–RM11.29bil). Simply put, this means that any foreign funds that came in ten years ago have already left.

“This includes those that have come in much earlier before, hence the negative number. With a huge chunk of foreign funds gone, there are likely not many other major sources of sellers left in the market, ” says Wong.

Wong says that in the aftermath of the panic selling, value is emerging.

In terms of valuation, we are considered undervalued now. The local index is now priced at (-2x) standard deviation below its ten-year mean in terms of price-earnings (PE) and price-to-book (PB) ratio.

“Some blue-chip stocks which are your everyday household names are trading lower compared to 10 years ago and some, even lower compared to 20 years ago.”

Thus in short, Wong says markets are already pricing in crisis-level valuations.

“We do not think a financial crisis is on the horizon yet, based on economic indicators and data and as global central banks continue to pump-prime to support their respective economies. This looks more like a crisis of sentiments and the ensuing panic, ” says Wong.

Nonetheless, it remains to be seen whether these valuations will hold, considering earnings in the upcoming reporting quarters are likely to take a huge beating.

Meanwhile, Yoong opines that the Covid-19 pandemic will most likely persist into the fourth quarter of 2020.

“The market will stabilise when there is a reliable and effective way of testing for those afflicted by Covid-19. At the current fast rate of progress, this could be by June 2020.

“The capital markets are more concerned with the economic and financial costs of Covid-19 than the health implications. The order of importance is therefore testing, prevention and cure, from the capital markets standpoint, ” says Yoong.

Strategy to invest

Yoong knows it is very difficult to time the market as there has been lots of emotion doing it.

“Best decisions are made when there is little emotion and made on the facts available. This is the worst time to sell.

“If you do not need to liquidate any stock positions, don’t.

“My investment strategy is to invest in listed companies that have well-managed and financially sound sustainable businesses. The recent collapse in share prices is therefore a big bonus. I will buy 10% to 20% tranches of the total amount over a period of one to three months. This is the winning formula, ” says Yoong.

For those who are looking to get into the market, Khoo says there are two clusters of stocks that would be more resilient, quicker to recover and thereafter sustain at higher valuations.

They are the high dividend yield stocks, whose yields have become more attractive especially with the selldown. Eventually, the search for yield will return (amid an exceptionally low interest-rate environment).

“When sanity returns, valuations in these stocks will swiftly improve, ” says Khoo.

The other cluster of stocks are the exporters, particularly those in the electrical and electronics sector.

“With the ringgit still heading south, margins will also rise. However, this strategy requires tolerance to high volatility, ” concludes Khoo.

Source: The Star