If you want a 95% probability of stocks outperforming bonds, you better plan on 20 years

Published: May 19, 2020 at 6:34 p.m. ET, By Mark Hulbert

With U.S. stocks having recovered from its March waterfall decline to within 13% of its Feb. 19 all-time high, many are wondering if it’s safe to step back into the market.

In fact, some brokers are now enticing investors with visions of another bull market run like the one that began in March 2009, the longest in U.S. market history.

Those visions may come to pass, but you’re in for a long wait. In fact, only if you’re willing not to touch your money for 10 years — until 2030 — should you even think of putting new money into the stock market right now.

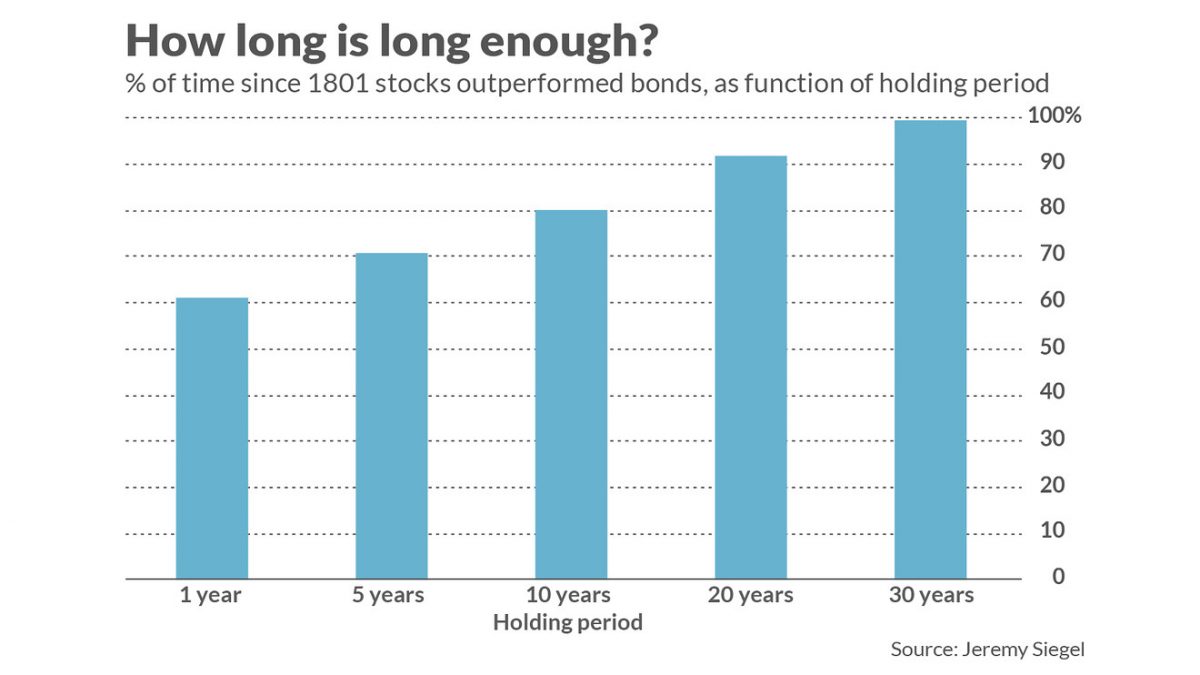

I say this not because I think it will take that long for the S&P 500 SPX to recover from the coronavirus pandemic. My advice instead derives from the historical odds. After holding stocks for at least 10 years, you have an 80% chance of outperforming bonds. If a one-out-of-five chance of lagging bonds is still too high, you need to be prepared to leave your equity investments untouched for even longer than 10 years.

Consider the percentage of times since 1801 in which the U.S. stock market outperformed bonds, as calculated by Jeremy Siegel, the finance professor at the Wharton School of the University of Pennsylvania and author of “Stocks For The Long Run.”

For example, as you can see from the chart below, stocks have outperformed bonds in 71% of all rolling five-year periods since 1801. Even on the assumption that the future will be like the past, a generous assumption as I have argued elsewhere, that means there’s a 29% chance that the money you put into the stock market today will not outperform bonds over the next five years. With bond yields currently so low, that is a disheartening prospect indeed.

I focus on five years because many advisers and financial planners default to that holding period when pressed for the minimum length of time investors need to leave untouched any money they put into the stock market. But a 29% chance of lagging bonds is unacceptably high.

What if you want a 95% probability of stocks outperforming bonds? That’s the threshold statisticians frequently use to determine if the odds of failure are acceptably low. As you can see from the chart, the lesson of the past two centuries is that you must be willing to hold your investments for more than 20 years.

When confronted by these statistics, some would argue that the odds of stocks beating bonds in coming years surely must be higher than what I am presenting here, since current bond yields are so low. But the data don’t necessarily back up this argument. Though bonds’ long-term prospects currently look mediocre at best, the same goes for the stock market (as I argued in a recent column).

What if stocks’ prospects are overstated?

Sobering as these statistics are, they may very well overstate the odds of stocks outperforming bonds. That’s the conclusion of research conducted by Edward McQuarrie, a professor emeritus at the Leavey School of Business at Santa Clara University who has painstakingly reconstructed bond market returns back to 1793. He found that bonds in the 19th century performed significantly better than previously estimated.

The table below summarizes what McQuarrie found for 20-year holding periods back to the late 1700s. (Note that he considers that bonds and stocks tie when the difference in their annualized returns is less than half a percentage point.)

| ALL 20-YEAR PERIODS ENDING BETWEEN… | BONDS BEAT STOCKS | STOCKS BEAT BONDS | BOND AND STOCKS TIE |

|---|---|---|---|

| 1813-1900 | 51% | 29% | 20% |

| 1901-2013 | 5% | 81% | 14% |

As you can see, the lesson you draw from U.S. history depends crucially on which period you focus on.

The bottom line? When reassuring yourself that the long run will bail out your stock portfolio, be sure you’re genuinely focusing on the long run. Don’t be as short-term oriented as some on Wall Street, where a running joke is that the long term lasts from lunch until dinner.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

More: This settles the stock-market valuation dispute between billionaires David Tepper and Nelson Peltz

Source: www.marketwatch.com